Table of Contents

Introduction

Managing your finances efficiently is crucial for achieving financial well-being. Yet, many people find themselves struggling to strike a balance between covering daily expenses and working toward long-term goals. Financial security is not simply about having enough money for today—it is about creating a sustainable plan supporting your future ambitions and providing resilience for unexpected emergencies. With the right strategies in place, it becomes possible to stay on top of bills, steadily progress toward your dreams, and respond confidently to life’s financial surprises. For those moments when you need extra flexibility, options like MaxLend loans can serve as a resource for short-term necessities. However, using credit or loans should be a backup—sustainable budgeting is always the best foundation for long-term financial peace of mind. By developing solid habits, you will reduce stress and be ready to tackle new opportunities as they arise.

Below, you’ll find a comprehensive and practical guide to managing your money. It draws on proven approaches to help you regain control and enjoy greater freedom with your finances. Whether you’re just starting or looking to fine-tune your system, these tips offer actionable steps to build a future where your financial decisions are intentional and stress-free.

Track Your Expenses

Understanding where your money goes is the first building block in budgeting success. You can’t fix what you don’t track, so spend at least a month recording every expense—no matter how minor. From your morning coffee to monthly streaming services, keeping a detailed record provides a clear, honest picture of your spending habits. Many are surprised by how quickly small, frequent purchases add up. Digital tools such as budgeting apps or spreadsheets make expense tracking easier and can categorize spending, providing charts or reports for quick analysis. This information highlights areas where money might be slipping away unnoticed and helps you identify opportunities to adjust habits quickly. If tracking every expense feels overwhelming, try starting with just one category, such as dining or groceries, for a week or two before expanding.

Set Clear Financial Goals

Setting realistic, specific financial goals is a powerful motivator and gives your budgeting efforts direction and purpose. Consider what’s most important for your future, whether establishing an emergency fund, paying off credit cards, buying a new car, or saving for travel. Break each large goal into smaller, more manageable targets—like saving $50 a week or reducing credit card balances by $100 each month—which makes progress measurable and the process less daunting. Make your goals visible by writing them down or creating a vision board to help keep them top-of-mind. Prioritize these goals based on urgency and importance. For example, building an emergency fund typically takes priority over discretionary spending. With clear, broken-down milestones, you can monitor progress, stay motivated, and celebrate achievements—no matter their size.

Choose a Budgeting Method

Different budgeting methods suit different personalities and lifestyles, so picking one that resonates with you is crucial. Here are three popular approaches to consider:

- 50/30/20 Rule: This framework suggests allocating 50% of your income for essentials, such as rent and groceries, 30% for wants, such as dining out or entertainment, and 20% for savings or debt repayment. It provides a balanced approach to spending and saving, making it simple to implement and adjust as your income or needs change. For a thorough explanation, see this detailed guide on the 50/30/20 rule.

- Zero-Based Budgeting: In this method, every dollar of your income is assigned a specific job, be it covering a bill, adding to savings, or funding entertainment. At the end of each budgeting cycle, your income minus expenditures should equal zero. This approach maximizes control, reduces money leaks, and ensures you are accountable for every cent.

- Envelope System: This classic, cash-based system involves assigning physical cash to specific categories, such as groceries, transportation, or entertainment, and using only what’s in each labeled envelope throughout the month. When an envelope is empty, no more money is spent in that category, making it an excellent tool for those prone to overspending in particular areas.

The most important factor is consistency. Whichever method you choose, stick with it for a few months and refine your system as necessary.

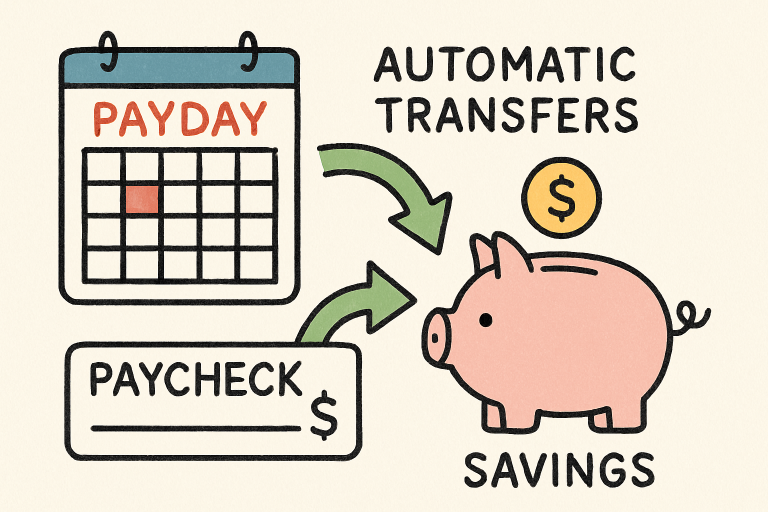

Automate Your Savings

Cultivating a habit of saving is much easier when it becomes part of your routine, the same way rent or utility payments are. Automating your savings removes the temptation to spend first and save what’s left. Set up automatic monthly transfers to a dedicated savings account right after payday, treating your savings as a non-negotiable expense. Automation also provides peace of mind by ensuring you’re steadily and consistently progressing toward your goals, regardless of how busy or distracted life becomes.

Some banks offer high-yield savings accounts or options to create multiple savings “buckets” for different purposes (like vacations, holiday shopping, or car repairs). Automating contributions to each goal ensures you prepare for expected and unexpected needs. If you receive extra income—such as a tax refund or bonus—increase your automated deposits to boost your savings without adding more work.

Reduce Non-Essential Spending

Eliminating or reducing discretionary expenses is one of the quickest ways to boost your savings and free up money for priority goals. Start by carefully examining your regular spending for areas you can cut back. Brew coffee at home instead of buying it daily, pack lunches, cook dinners more frequently, or explore free community events for entertainment. Review subscriptions and memberships—cancel or pause those you rarely use. Many are shocked at how much they spend on convenience or impulse buys each month.

A key to reducing non-essential spending is consistently evaluating wants versus needs. Before every purchase, ask yourself whether it aligns with your priorities and financial goals. If not, consider waiting 24 hours before buying—this “cooling off” period helps reduce impulse buys and often results in more thoughtful decisions. Remember, minor adjustments compounded over weeks and months can turn into significant savings, easing financial pressure and speeding your path to larger goals.

Plan for Irregular Expenses

Not every expense fits neatly into a monthly budget. Irregular costs—such as annual insurance premiums, car repairs, holiday gifts, or unexpected medical visits—can disrupt your finances if you’re unprepared. To stay ahead, consider creating a sinking fund, a separate savings account specifically for these periodic expenses, and contribute regularly. For instance, if your car insurance costs $600 annually, setting aside $50 per month prepares you in advance. This strategy helps you avoid last-minute scrambles or relying on high-interest credit. When extra support is needed, a short-term option like a MaxLend loan can offer quick relief—especially since you can apply online for added convenience. By combining proactive saving with flexible financial tools, you can maintain control over your budget and reduce unnecessary stress.

Review and Adjust Regularly

Your financial situation and goals are not static—they change as your life does. A new job, a growing family, or a shift in priorities often requires a fresh look at your spending plan. Make it a habit to review your budget at least monthly or quarterly. Check your progress toward previously set goals, reevaluate what’s working, and identify areas where you may need to tighten spending or reallocate funds. An ongoing review process keeps your budget relevant, realistic, and practical, and ensures you always make the most of your money, no matter what life brings. It also allows you to spot problematic patterns early and make the necessary changes while they are still manageable.

Involve Your Family

Budgeting produces the best results when everyone in your household is involved. Transparent conversations about goals, spending decisions, and responsibilities create a shared sense of purpose. Assign specific roles to family members—for example, put someone in charge of tracking grocery expenses or brainstorming creative ways to save on entertainment. Family meetings to discuss progress can help reinforce smart financial behaviors in children and provide encouragement to all household members. Working together makes managing money more effective and strengthens trust and unity within your family. Celebrate big and small successes to keep everyone motivated and engaged as you strive for a more secure future together.

Embracing these budgeting strategies will help you create a lasting foundation for financial health. Remember, significant change comes through small, consistent steps—by making wise choices day after day, you’ll find that your daily needs and future dreams soon become well within reach, and financial stress is replaced with confidence and peace of mind.